Report Overview:

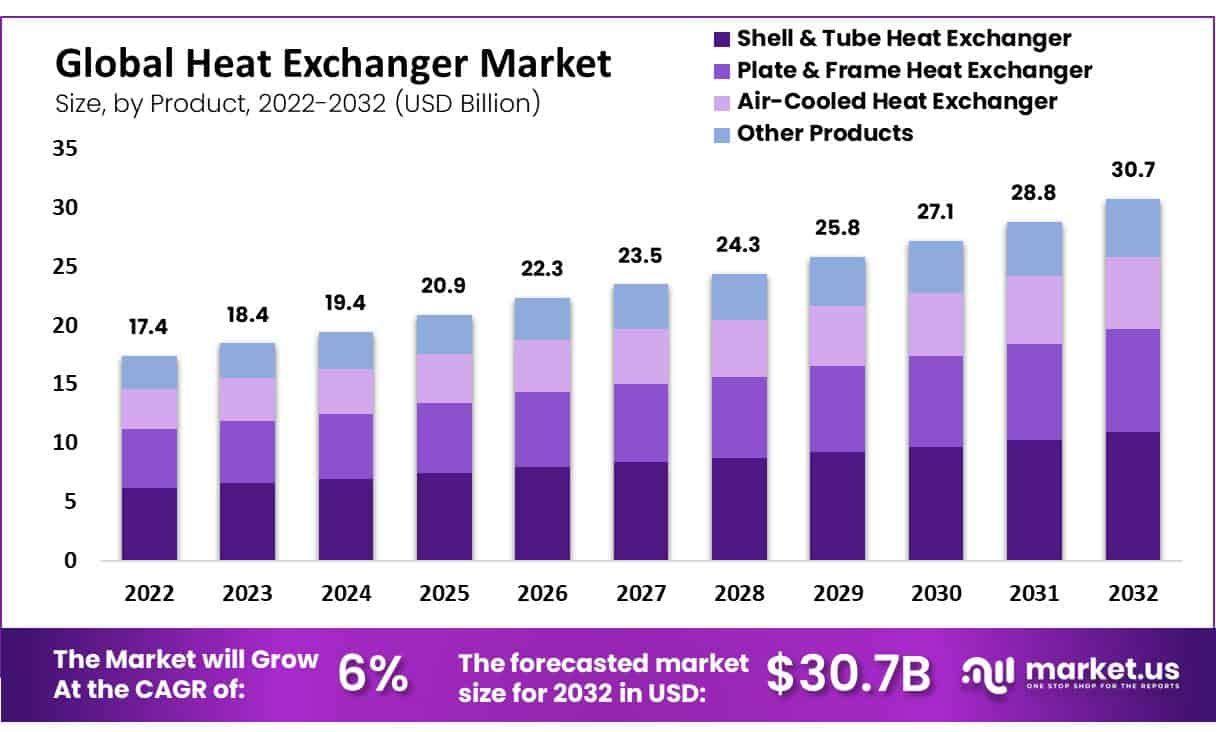

The global heat exchanger market was valued at approximately USD 17.4 billion in 2022 and is forecast to grow at a 6% CAGR from 2023 to 2032, reaching around USD 30.7 billion by 2032. Demand is being driven by key sectors such as oil & gas, power generation, chemical processing, HVAC, and food & beverage highlighting the growing global emphasis on efficient thermal management

Key Takeaways

- Shell & tube exchangers dominated in 2022, contributing 35.7% of market revenue.

- Chemical & petrochemical industries led end-user demand with ~22.7% share.

- Rising energy prices and the expansion of renewables are major growth drivers.

- Obstacles include high initial costs and complex manufacturing processes.

- Opportunities lie in the rapidly growing demand from developing nations and the increasing shift toward energy-efficient exchangers.

- Regional strength: Europe held about 31.9% of the global market in 2022.

Sample Report Request For More Trending Reports:

https://market.us/report/heat-exchanger-market/free-sample/

Key Market Segments

Based on Product

- Shell & Tube Heat Exchanger

- Plate & Frame Heat Exchanger

- Brazed Plate & Frame Heat Exchanger

- Gasketed Plate & Frame Heat Exchanger

- Welded Plate and frame Heat Exchanger

- Others

- Air-Cooled Heat Exchanger

- Other Products

Based on the Material of Construction

- Stainless Steel

- Copper

- Aluminum

- Other Materials

Based on End-User

- Chemical & Petrochemical

- Oil & Gas

- HVAC & Refrigeration

- Power Generation

- Food & Beverage

- Pulp & Paper

- Other End-Users

Product Analysis

In 2022, the shell & tube segment dominated the market, accounting for 35.7% of the total revenue demand. A shell & tube product is made from a bundle or tubes that are placed inside a cylindrical shell. The tube axis is parallel to the shells.

There are three main types of shell and tube products including U-tube design, fixed-tube sheet design, and floating-head design. Shell and tube products can be used for applications that require high temperatures & pressures.

They also transfer between liquids, liquids & gas. The plate and frame segment grew at a CAGR of 5.6% during the forecast period. The plates used to make plate-type exchangers are available with corrugation & smoothness. Air-cooled products are made up of a tube bundle, an air-pumping device like a fan, axial flow, or blower.

Material of Construction Analysis

The heat exchanger market was dominated by the steel segment. Owing to its durability and strength as well as resistance to corrosion, stainless steel is ideal for heat exchanger contraction. Mild steel and stainless are the most popular steel grades. It has many benefits like its corrosion resistance at a range of pH levels and its lightweight & high thermal conduction.

It can also be utilized with normal clean water, without needing to use special fluids. It is a bit expensive, but the characteristics above make it an excellent choice for long-term use.

End-User Analysis

The market was led by chemical & petrochemicals, which accounted for 22.7% of global revenue demand in 2022. Because of their design flexibility and corrosion resistance, heat exchangers are widely used in the chemical processing sector. They can handle fluids with different levels of solids owing to their properties.

The demand for heat exchangers will increase at a CAGR of 4.7% in the oil and gas industry over the forecast period. Heat exchanger demand will increase owing to the increased use of shale for manufacturing and energy as well as the technological advancements in exploration which are anticipated to increase shale exploration. Industrial growth will also be driven by the rising number of oil and gas projects in different nations.

infoTo learn more about this report – request a sample report PDF

infoTo learn more about this report – request a sample report PDFKey Market Segments

Based on Product

- Shell & Tube Heat Exchanger

- Plate & Frame Heat Exchanger

- Brazed Plate & Frame Heat Exchanger

- Gasketed Plate & Frame Heat Exchanger

- Welded Plate and frame Heat Exchanger

- Others

- Air-Cooled Heat Exchanger

- Other Products

Based on the Material of Construction

- Stainless Steel

- Copper

- Aluminum

- Other Materials

Based on End-User

- Chemical & Petrochemical

- Oil & Gas

- HVAC & Refrigeration

- Power Generation

- Food & Beverage

- Pulp & Paper

- Other End-Users

Driving Factor

The market will be driven by the increasing industrialization of developing countries.

According to the enormous development taking place in APAC nations like China and India, it is anticipated that the market for heat-exchanging equipment will increase. The reasons for this include rising raw material prices as well as the cheap cost of labor. The low cost of labor and rising prices for raw materials are too responsible.

The success of regional industrial, commercial, and manufacturing projects has contributed to the overall growth of global heat exchangers. The demand for heat exchangers is increasing owing to raised demand from the chemical & HVACR sector as well as government initiatives in India and Japan for developing thermal & solar energy. The heat exchangers market will also benefit from the anticipated rise in demand for petrochemical products.

Restraining Factors

Impact of fluctuating raw material prices on heat exchanger manufacturers

Heat exchanger manufacturers can be affected by the volatility of raw materials prices, such as steel, aluminum, and copper. The volatility of raw material prices affects manufacturers owing to many factors like economic conditions & exchange rates.

Price fluctuations may cause delays or cancellations in large capital projects, which could negatively impact the growth of heat exchangers. Pricing trends are closely monitored to manage price fluctuations risk and minimize their impact on pricing.

Opportunity

Growing nuclear power plants to drive the heat exchangers market

The overall efficiency and output of a nuclear power station’s nuclear power plants are affected by heat exchangers. Heat exchanger manufacturers have key opportunities in the market for new projects & increased use of heat exchanging units in nuclear reactors.

There is a lot of growth opportunity in the heat exchanger market across many industries, including chemical, petrochemical, and HVAC. Heat exchangers are essential components of many industrial processes because they can transfer heat between fluids and gases.

Trends

Rising Demand for Energy-Efficient Solutions: The demand for energy-efficient solutions is growing. With an increasing focus on energy efficiency, sustainability, and various industries there is the fastest need for heat exchangers that are energy-efficient. Heat exchangers that are more efficient, use less energy, & emit less carbon dioxide have been developed by manufacturers.

Adoption of compact heat exchangers: Compact heat exchangers are becoming more famous because of their lighter weight, smaller footprint & better performance. These heat exchangers have huge heat transfer rates & reduced fouling when compared to traditional heat exchangers.

Heat Exchanger Market Growth: Development of Advanced Materials. The market is expected to grow due to the development of advanced materials, such as superalloys, ceramic composites, and graphene. These products have improved heat transfer properties and higher strength when compared to traditional materials.

Regional Analysis

In 2022, Europe will dominate the global market with a share of 31.9%. The public & private sectors will continue to invest in infrastructure, which will drive the need for these products. During the predicted period there will be a growing demand from different end-use industries for heat exchangers that are more durable, efficient, & have less fouling. North America will see a high demand for these products due to increased oil and natural gas exploration in the U.S. & Canada.

The market for heat exchangers will benefit from the growing energy requirement in various commercial and industrial segments. Asia Pacific’s heat exchanger market will grow by 6.2% over the forecast period. This market growth has been driven by the faster industrialization of Asia Pacific’s developing nations and increasing investments in industrial and commercial projects. China’s heat exchanger market will be driven by the growth of investment in the HVAC, chemical, and petrochemical industries.

Growth Opportunity

- Compact & energy-saving designs: Manufacturers are focusing on smaller, more efficient units that reduce energy use and carbon emissions .

- Advanced construction materials: Adoption of stainless steel, alloys, and composites (like ceramic) is rising to enhance performance and durability .

- Emerging markets: Rapid infrastructure and industrial growth in APAC, especially China and India, offer high potential .

Latest Trends

- Efficiency first: Industry shift toward heat exchangers that are more compact, more efficient, and lower in CO₂ emissions.

- Material innovation: Development of superalloys and composites, as well as advanced brazing and gasket technology to enhance life span and performance .

- Renewable sector uptake: Growing use within renewable energy projects, including thermals, nuclear plants, and heat pump systems .

Market Key Players

- Alfa Laval AB

- Kelvion Holding GmbH

- Danfoss A/S

- API Heat Transfer Inc.

- Xylem Inc.

- HRS Heat Exchangers Ltd.

- Hisaka Works, Ltd.

- Koch Heat Transfer Company

- GEA Group AG

- SWEP International AB

- Thermax Limited

- Tranter, Inc.

- Other Key Players